Tenure refers to the manner in which property ownership is held, referring to either leasehold (LH) or freehold (FH) property. This article seeks to debunk the myth of freehold residential properties being the preferential choice over leasehold properties for the purpose of profitability in the context of Singapore.

LH tenure gives the property owner the right to use and occupy the property for a specific period, primarily 99 years or 999 years in Singapore, before its ownership is reverted back to the state, without compensation. What happens upon expiry of the development’s lease is either:

Reversion without compensation

LH owners pay a land premium to the Singapore Land Authority (SLA) to extend the duration of the lease (approval subject to SLA’s discretion), or

Owners sell their property to a third-party developer (en-bloc sale) via 80% share value or strata area vote (10 years or older development) or 90% share value or strata area vote (less than 10 years). On top of this, enbloc usually only happens when developers see the profit potential of the land location and neighborhood.

On the other hand, FH tenure gives the property owner the right to use and occupy the land and the building in perpetuity, without the fear of reversion, future premium payments for a lease extension, or the non-guarantee of enbloc. With all this in mind, would freehold tenure condos be the preferred and more profitable choice for buyers? In reality, the tenure’s interactions with other factors result in the ideal choice for investment is not so clear-cut.

The profitability of residential properties generally come from 3 areas: realized capital gains (buying low and selling high), rental yield (low cost, high income), and occasionally en-bloc proceeds (which will be covered in another article). So where does tenure fit into the equation relating to the first 2 areas? We’ll look at rental yield which is more clear-cut than the more controversial realized capital gains.

Rental Yield

[Rental income per year / property price] * 100% = Rental Yield

Source credit: 99.co

Source credit: 99.co

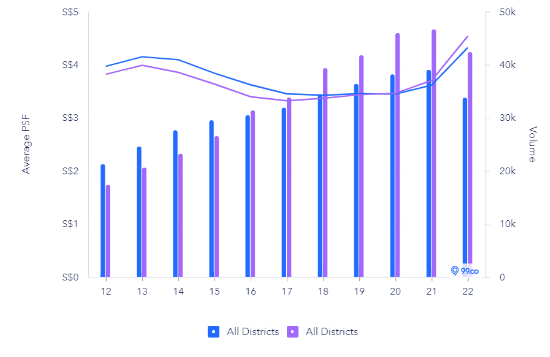

When it comes to rental yield, there is a clear winner. From the above table, we can see that average rental yield is very close between both tenures, but since 2020, even the 99-year LH is beating out FH in terms of yield. The reason is simply due to the fact that tenants do not care about tenure (unless it is very close to expiry).

What tenants do care about are:

Price

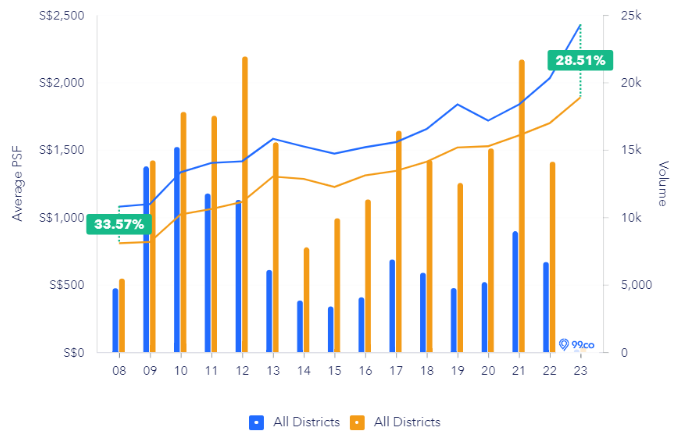

Here, you can see a graph comparing the average price of FH vs LH condominiums since 2008. The blue line represents FH Condominium Developments and the yellow line represents LH Condominium Developments, including both 99 years and 999 years.

Source credit: 99.co

When it comes to price, all else being equal, FH condominiums cost 10-15% more than LHs due to the freehold premium that has already been calculated into its initial cost, since all FH developments do not have the downsides of LH development’s depreciation caused by the limited tenure (mentioned above). This lowers the cost of LH units which increased the overall yield percentage.

Facilities

At the same time, rental yield for LH condominiums has been increasing and even surpassing that of FH, despite the lower initial cost. This is because the Singapore government has long stopped releasing freehold titles under Government Land Sales due to land scarcity. With improved landscapers, architects, as well as larger land plots allowing for LH developers to exploit economies of scale, this means that the newer condominiums with new, larger and higher quality swimming pools, gyms and playgrounds, tend to come from LH condominiums, for which tenants are more willing to pay a premium.

That said, rental yield is only a part of determining profitability. Let’s take a look at how the tenures fare based on capital gains.

Capital Gains

Overall there are arguments for both sides being a better investment choice.

Why FH might be a better choice

Although LH properties have generally been more profitable than FH properties when looking at appreciation starting from 2008, you can chalk it up to the quantum of the initial price of LH properties being low enough that it reflects a higher percentage change compared to their FH counterparts. What is certain, however, is that LH land value drops over time.

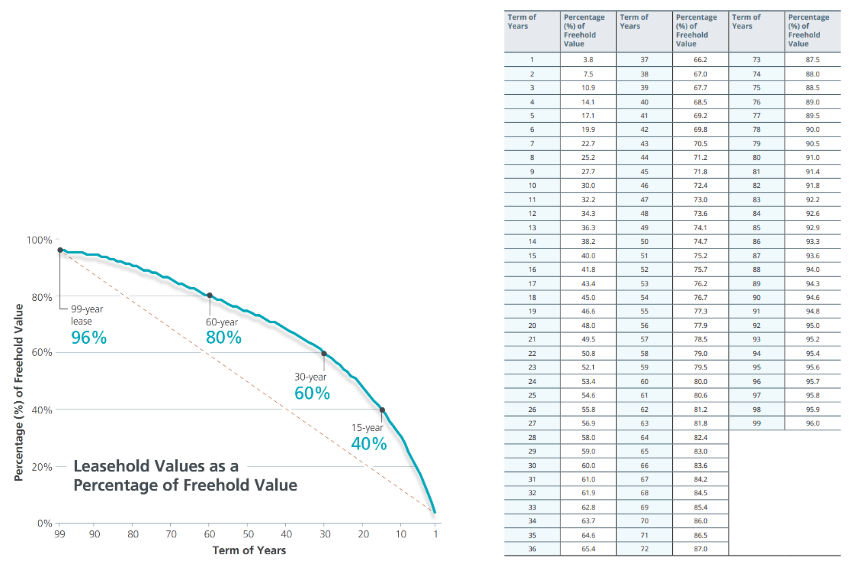

The Bala table shows the drop in LH land value as a percentage of FH land over time. As can be seen from the curve, LH land value drops very slightly but accelerates as tenure reaches the 60-year, 30-year, and eventually 15-year mark. This tells us that given the same property aside from tenure, there is a significant impact on LH property value the closer its tenure is to expiry.

The scarcity of new FH land (only attainable through en-bloc sales) could result in higher perceived or even actual value. In fact, for 99yr LH condos, banks tend to tighten loan limits after 40 years from launch, and once there are 30 years or less left on its lease, CPF can no longer be used to finance the property, leading to policy restricted demand on older 99yr LH condos.

Why LH might be a better choice

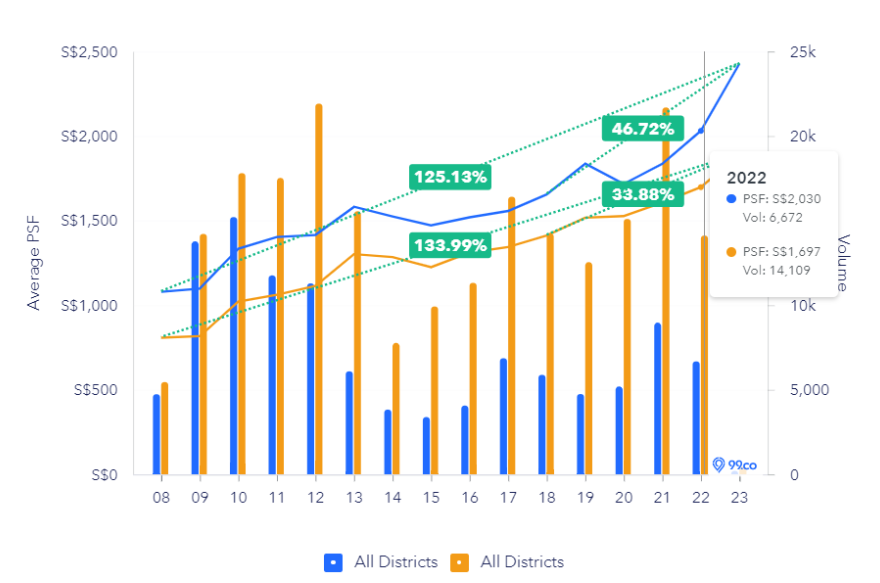

When you look at appreciation from the last 5 years, it seems that FH Condominium outperforms LH by a significant margin (38% higher % increase). In actuality, this significant difference can also be chalked up to the relatively low transaction volume available in 2023.

Source 99.co

As can be seen, the average price in 2022 is spread across 6.6k FH and 14k LH transactions, whereas the average price in 2023 (only the month of January) is spread across 190 FH and 450 LH transactions, making it a lot less determinative of tenure performance, and when you look at the performance of tenure from 2018 to 2022, they are in fact neck and neck.

Source 99.co

Another issue that has been frequently overlooked is the volatility of prices in FH developments.

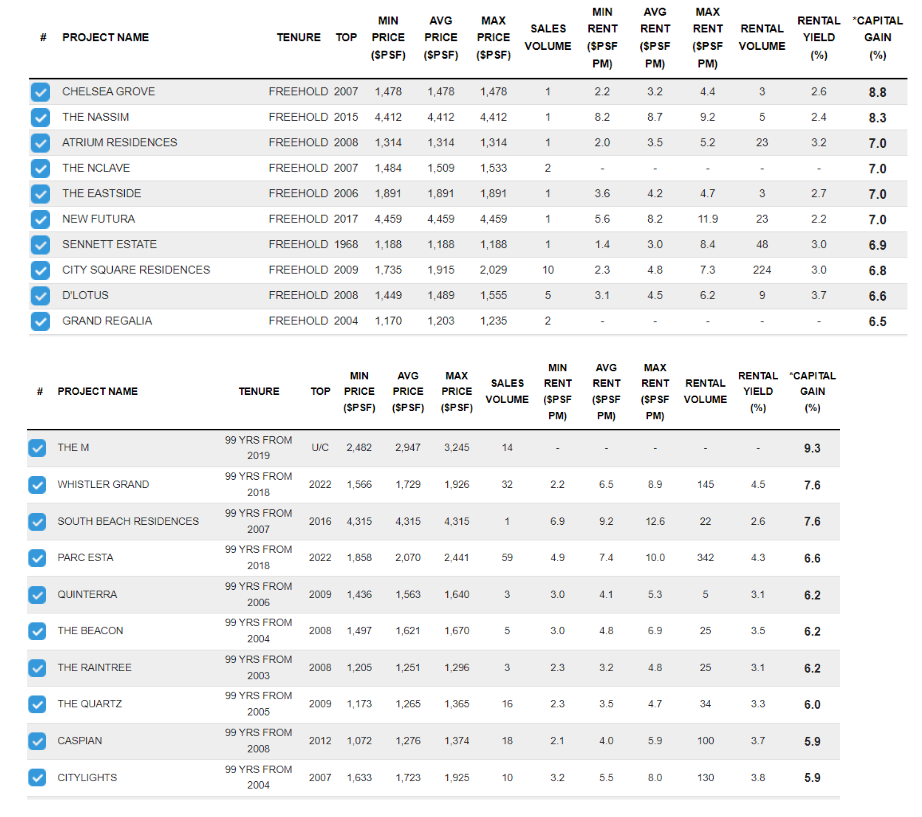

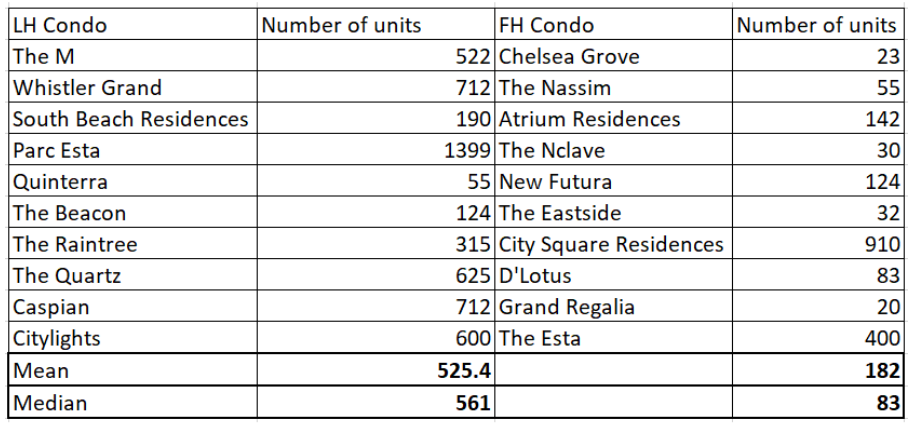

The first table shows the top 10 performing FH condos while the second table shows the top 10 performing LH condos as of 2023 (capital gains). The table below shows the number of units in each of these top 10 developments

There is a clear difference in transaction volume between LH and FH Condos, with LH having 3 times the number of units and transactions as that FH. The reason for this is that the plot ratio has been increasing in recent years, particularly for LH condominiums, which allows for more units to be built within a particular plot. Furthermore, as previously mentioned, new land for Condominiums being released will only be for leasehold developments (the only new land available for FH condos will come from en-bloc). Consequently, low transactions may artificially inflate FH condominium prices, making it less clear that, in the short term, FH condominiums will outperform LH condominiums, especially when the Freehold premium is already calculated into its price from the outset.

Conclusion

In my opinion, when it comes to overall profitability due to tenure considering capital gains and rental yield, the preferred choice depends on the investor’s timeframe. If the investor is looking to exit within 5 – 7 years from launch, depreciation caused by tenure will have a much lower impact on LH land value, alongside higher rental yield from the novelty and quality of facilities and lower property price. On the other hand, the Bala curve also indicates that FH developments fare much better in 30 years than LHs with only a few years remaining. In the future, it is also likely, based on demand and supply theory, that FH developments become so rare in Singapore that eventually investors are willing to pay a much higher premium for it. The question then becomes when demand for FH caused by scarcity will exceed the premium paid for FH over LHs.

Written by: Caleb Phee | JNA Investment Analyst

Edited by: Jervis Isaiah Ng | Founder & Christian Oh | Director of Investments