Photo by Mike Enerio on Unsplash

What is the hike?

In the Budget Speech 2023 held on 14 February, the government announced that, to fortify Singapore’s fiscal position by generating an additional estimated $500 million in revenue per year, higher marginal Buyer Stamp Duty rates for higher-value residential and non-residential properties will be introduced. This is consistent with fiscal policies implemented last year, including raising the GST rate, Personal Income Tax rates for top income earners, as well as property tax rates for higher-value owner-occupied residential properties and all non-owner-occupied residential properties. As PwC Singapore’s real estate and hospitality tax leader Teo Wee Hwee said in the 2018 BSD hike: “This is not a property cooling measure; it’s a measure to collect more revenue, and in line with having a more progressive tax system.”

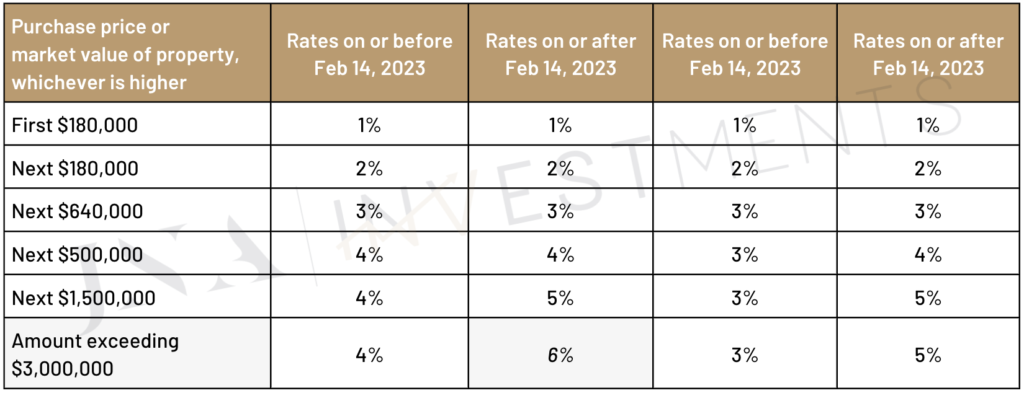

The stamp duty changes can be seen in the table below:

In essence, residential properties priced above $1.5m will be taxed 1% more up to an additional $1.5m, and thereafter 2% more than the original stamp duty rates. Non-residential properties priced above $1m will be taxed 1% more up to $500k, and thereafter 2% more than the original. These are the simplified calculations:

<1m: 3%-5400

1m to <1.5m: 4%-15400

1.5m to <3m: 5%- 30400

3m and up: 6%-60400

What does this mean for residential and non-residential investors?

Let’s take a look at what happened at the last stamp duty hike to gauge the potential impact of the stamp duty hike on property prices.

On 19 February 2018, it was announced that the top marginal Buyer’s Stamp Duty (BSD) rate for residential properties will be raised from 3% to 4%, applying to the portion of residential property value in excess of $1 million, constitutes a small portion of the HDB market and a majority of the private residential property market (average at $1.56m). There were no changes to stamp duty rates for non-residential properties.

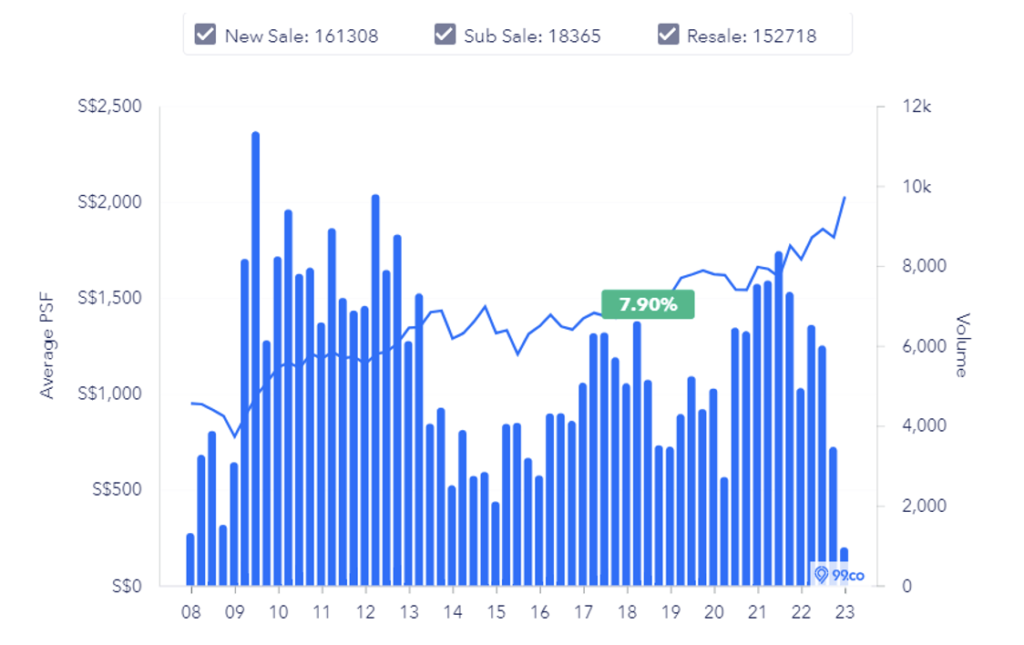

Condo prices during the previous stamp duty hike

Source: 99.co

Source: 99.co

Within 1 month of the stamp duty hike, average prices dropped by $1psf for Condominiums across the market and rose by 7.9% by the end of the year. Further, volume of transactions rose by 400 from February to March 2018, showing little to no signs of private property transactions slowing down.

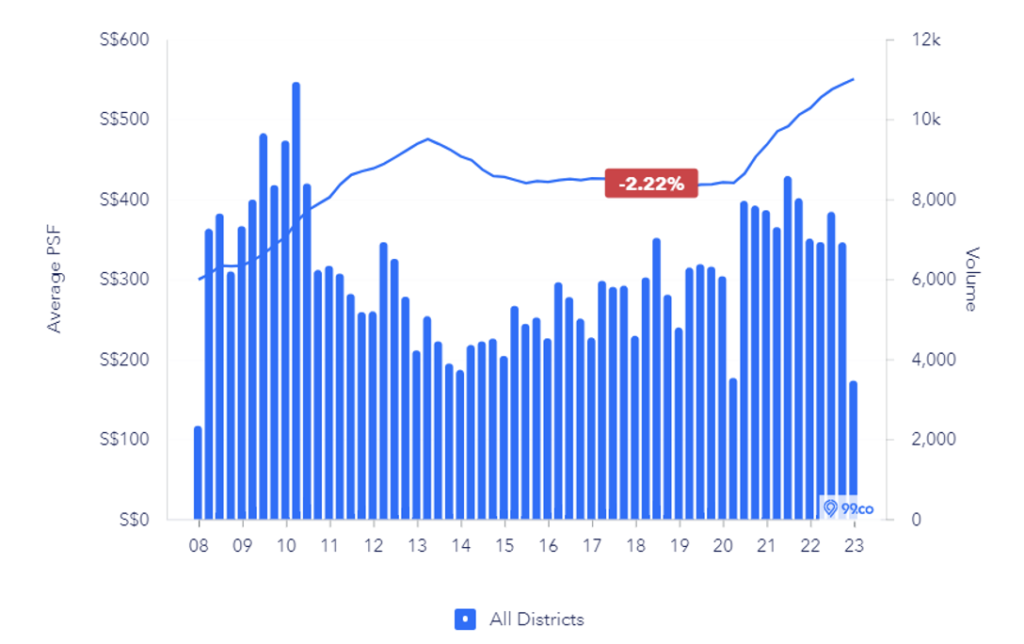

HDB prices during the previous stamp duty hike

Within 1 month of the stamp duty hike, average prices dropped by $1psf for Condominiums across the market and rose by 7.9% by the end of the year. Further, the volume of transactions rose by 400 from February to March 2018, showing little to no signs of private property transactions slowing down.

In contrast, HDB property prices stayed relatively stagnant and fell 2.2% by the end of the year. This comparison highlights that the stamp duty hike was not significant enough to effect a shift in buyers’ preference from private residential properties to HDB alternatives. This result is expected as it was not intended to serve as a blanket cooling measure but as a form of taxation on the wealthy for government revenue.

That said, the BSD hike increase this time around not only doubled at the pricier end (above $3m) for residential properties but also includes non-residential properties. As an example, the stamp duty payable for a $4m residential property will increase by $35000, and the stamp duty payable for a $2.5m commercial property will increase by $25000. Assuming an LTV of 75% and 80% for residential and commercial property respectively, initial capital outlay would increase by 3.5% (CPF included) and 5%.

The extent of cost increase for buyers of high-value residential property will unlikely deter demand given the strong fundamentals of the residential property market, while commercial property owners and businesses that are dependent on profit margins are likely to be affected. Developers will likely be affected the most as they may not only have to absorb the increased cost but also pay a heftier tax for en-bloc purchases where stamp duty is calculated on the total purchase price. Property Holding Entities and their shareholders are also likely to take a hit from the increase in additional conveyancing duty from 44% to 46%. As of today, the Straits Times Index had already fallen 1 percent while one of Singapore’s largest landlords City Developments had already fallen 2.8 percent. CapitaLand Integrated Commercial Trust, the largest real estate investment trust listed on the Singapore Exchange, saw a 2.04 percent drop, alongside Hongkong Land and Mapletree Logistics Trust which fell 1.8 percent.

So who’s the biggest winner of Budget 2023?

The biggest winners from Budget 2023 are likely HDB Resale Buyers that are not only unaffected by the BSD hike but also receive increases in CPF housing grants. Private real estate below $1.5m will likely be a more attractive investment alternative to pricier private residential properties, real estate stocks, and real estate investment trusts. As an individual property investor, it can also be worth considering residential property over commercial and industrial investments. Decoupling to purchase 2 lower quantum properties as opposed to 1 higher-value property subject to a higher stamp duty quantum can also be an option, although transaction costs still have to be taken into consideration.

Written by: Caleb Phee | JNA Investment Analyst

Edited by: Jervis Isaiah Ng | Founder & Christian Oh | Director of Investments