Source credit: The Continuum

In our last article, we analysed the viability of Tembusu Grand as an investment property. We came to the conclusion that it is a great choice for investment based on technical and fundamental analysis. Today we will discuss a similar D15 New Launch, The Continuum, making its debut on 15 April.

Freehold

Unlike its counterpart, the biggest difference in investment is that The Continuum is a freehold development. Some advantages of owning a Freehold Condominium are as follows:

-

Perpetual ownership: Freehold properties grant owners perpetual ownership rights, providing a sense of security and long-term investment potential.

-

Higher resale value: Freehold properties generally have higher resale values compared to leasehold properties, as they do not depreciate over time. More specifically, they are not subject to land depreciation caused by a limited leasehold period.

-

Flexibility in property usage: Freehold property owners enjoy greater flexibility in terms of property usage and renovations, as they do not need to comply with the restrictions imposed by lease agreements.

This article will explore in detail through both technical and fundamental analysis for what price The Continuum would be worth pursuing as an investment property and a projection for its future appreciation and rental yield. A more in-depth qualitative and comparative analysis can be made with other freehold condominiums in D15 to attain either a slightly higher or lower projection from the valuation.

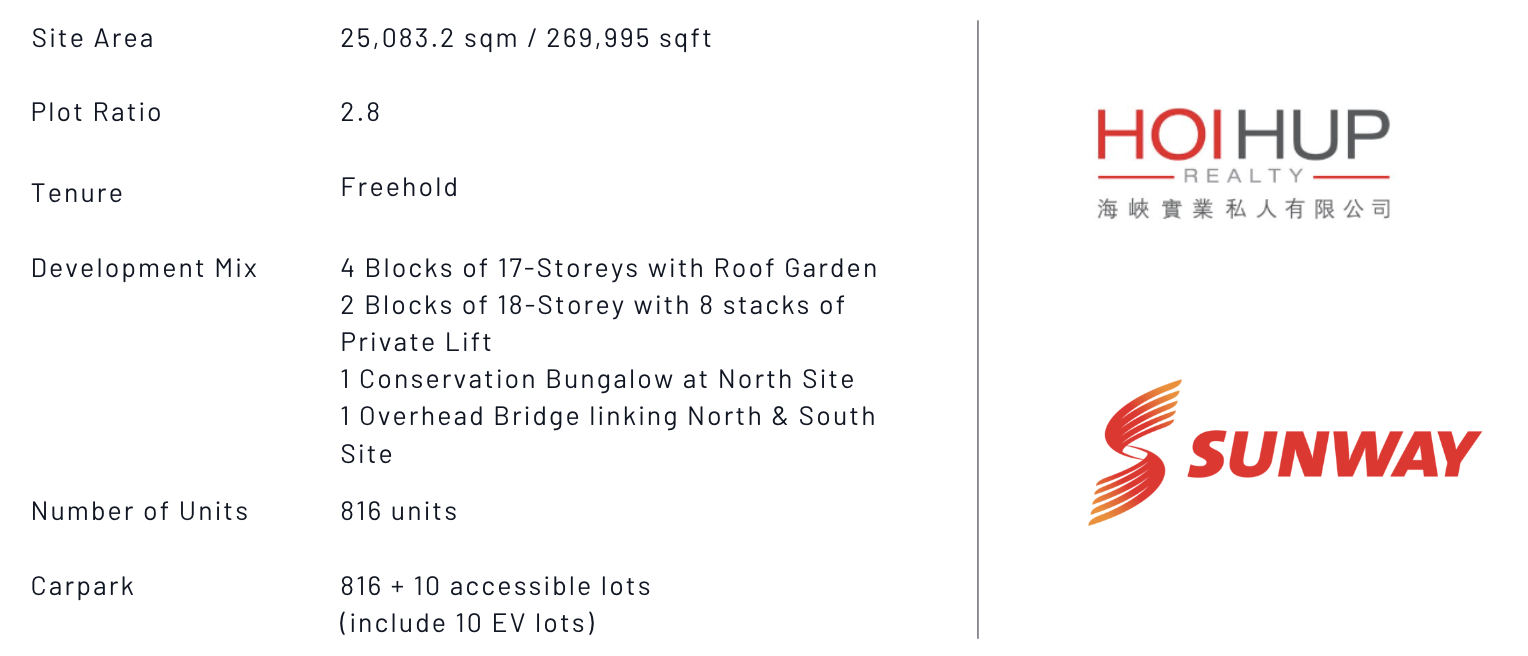

Basic Information

The Continuum is jointly developed by Hoi Hup and Sunway Katong Pte Ltd. Hoi Hup is a reputed real estate developer founded in 1983 with a portfolio of completed projects including over 50 developments with more than 10,000 homes built, with notable projects including Hundred Palm Residences, The Ford @ Holland, The Whitley Residences, and Sophia Hills, while Sunway Katong is a Singapore based subsidiary of the Malaysian Sunway Group, having developed Sunway Residences and Sunway Gateway Commercial Hub.

Technical Analysis

Estimate launch price based on comparative land bid breakeven and launch prices

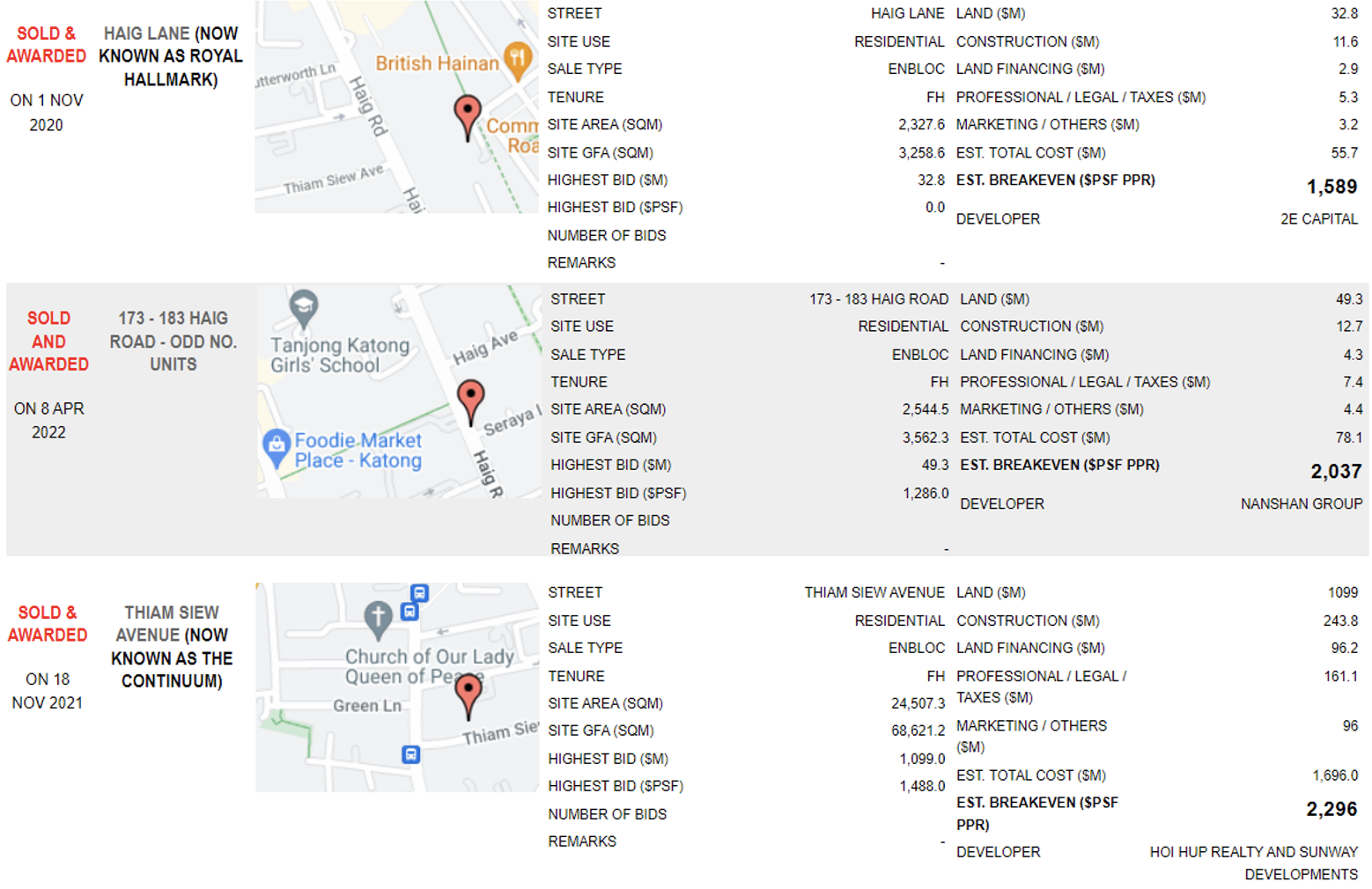

The purpose of the land bid price is to find a gauge for what is likely to be the launch price, as well as determine the rough threshold leeway for developers to drop prices subsequently should demand be lower than expected, as developers have to maintain a minimal profit margin. Here is a comparison of surrounding land bids and launch prices as well as Hoi Hup’s recent launch prices to estimate the average launch price of The Continuum.

Source credit: Onemap SG

Recent land bid and launch price comparison

-

2021 land bid: Thiam Siew Avenue (The Continuum) (FH), launching 15 Apr 2023.

-

2020 land bid: Haig Lane (Royal Hallmark) (FH), breakeven $1,589 psf, launched 2022, launch price average $1,867 (difference 17%, $278psf)

-

2017 land bid: Amber Park (FH), breakeven $2,171 psf, launched 2019, launch price average $2,483 (difference: 14%, $308 psf)

Latest Condo developments by Hoi Hup and Sunway Development

-

2021 land bid: Flynn Park (Terra Hill) (273 est units, FH), breakeven $2,079, launch price average $2,663 (difference: 28%, $584 psf)

-

2018 land bid: Brookvale Park (Ki Residences) (660 units, 999 yrs), breakeven $1,381, launch price average $1781 (difference: 29%, $400 psf)

-

2013 land bid: Mount Sophia (Sophia Hills) (493 units, 99 yrs), breakeven $1741, launch price average $2231 (difference: 28%, $490)

Given the consistency of Hoi Hup and Sunway’s pricing strategy, it is reasonable to estimate an average of around 28% difference between estimated breakeven price and launch price, with tenure being a non-factor for their pricing. Hence, it is likely that The Continuum will be launched at around $2938psf

How have these developments fared?

Terra Hill: As Terra Hill has only been launched last month in February, there is not enough data to determine if prices have gone up. As of March, there is only around 38% uptake, signifying weaker demand, potentially from fear of rising interest rates and economic instability.

Ki Residences: Although Ki Residences was initially sold at 29% above the estimated breakeven price at, it still appreciated to $2330psf (31% appreciation) after 3 years. A contributing factor would be the fact that despite the breakeven price gap is wide, the cost of the new launch is still lower than the average new launch price in the district (D21 Clementi) by $70psf.

Sophia Hills: On the other hand, Sophia Hills which was initially sold 28% above the estimated breakeven price, suffered a huge price cut of 14.67% from its initial launch price when developers found demand to be lacking, but prices subsequently picked up from that point in 2015.

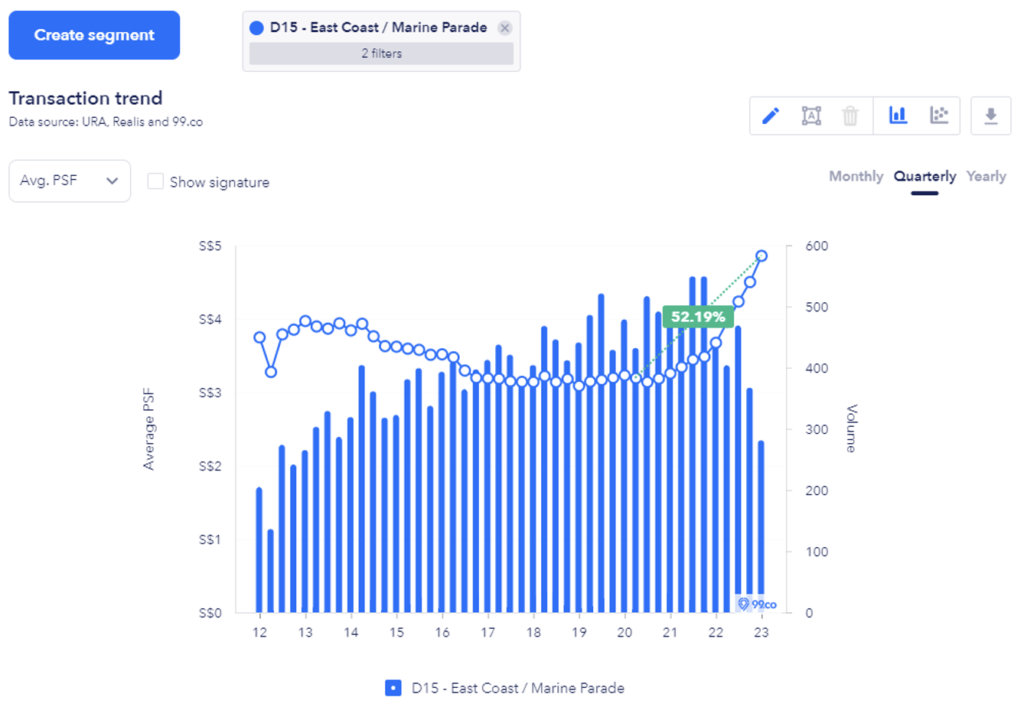

Source credit: 99.co

Source credit: 99.co

Estimated Capital Gain

For the purposes of estimating capital gains, each bedroom size will have its own analysis in order to avoid skewed average prices of developments as a result of differing bedroom size mixes.

Valuation method 1: Estimation based on average prices and completion date

This valuation method is applied by plotting a graph of average prices against the completion year (TOP date), for which we can find the estimated intrinsic value of the property unit for each unit type in the district based on when it is completed. The key is to purchase a unit at a reasonably below the estimated intrinsic value to enjoy capital gains.

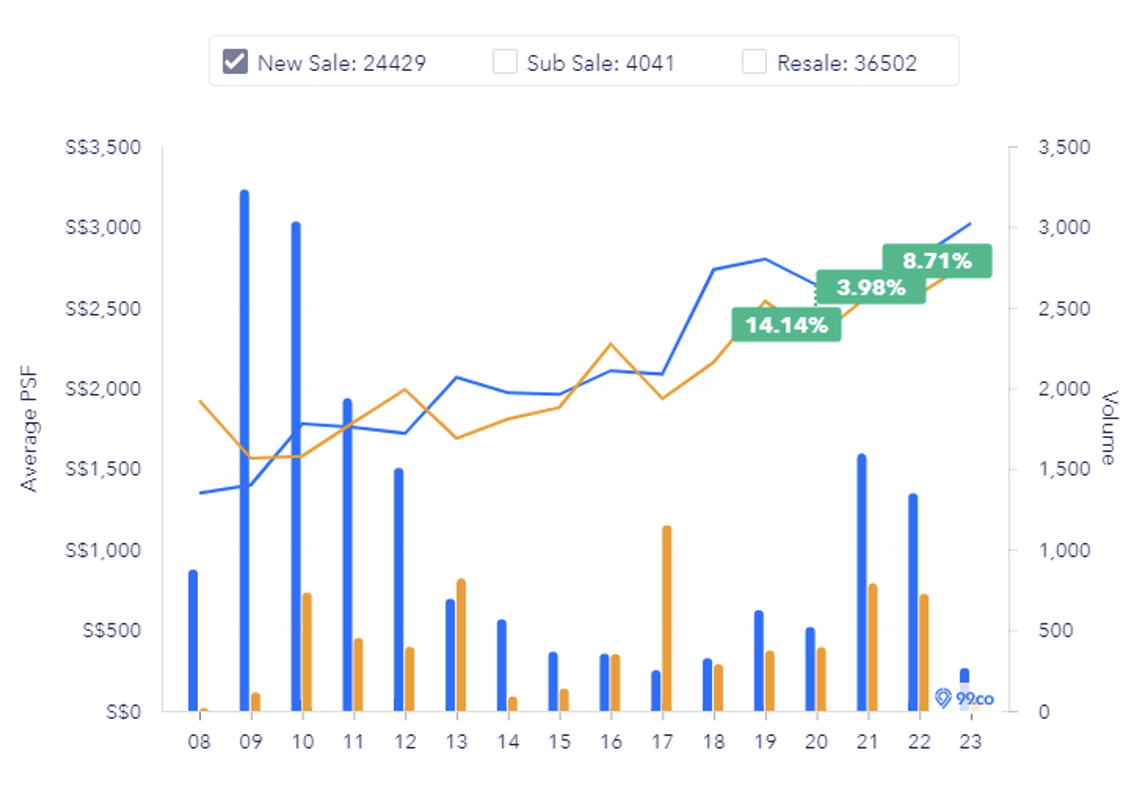

Firstly, we can estimate freehold premium by finding the 3-year average of the difference in average prices of 2BR with Freehold and 99yr leasehold tenure (for new sale). It is imperative to note the unique nature of D15 being overwhelmingly a freehold district, unlike some other areas, meaning that the premium buyers are willing to pay for a freehold tenure development in these areas are diminished. In order to more accurately measure freehold premiums in a district dominated by freehold Condos, the average district new sale prices of districts 9, 10, and 15 will be used.

Source credit: 99.co

Source credit: 99.co

Looking at the most recent 3-year average new launch prices for 99-yr and freehold condos, we can estimate the recent value of freehold premium in D15 to be:

(14.14% + 3.98% + 8.71%) / 3 = 8.94% (lower than the nationwide average freehold premium of 18.7%).

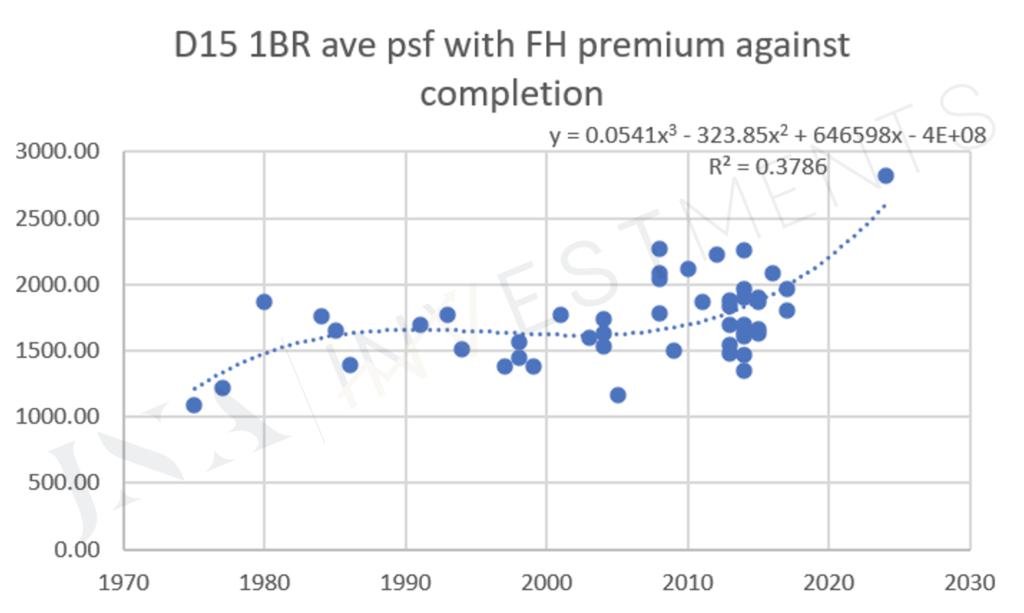

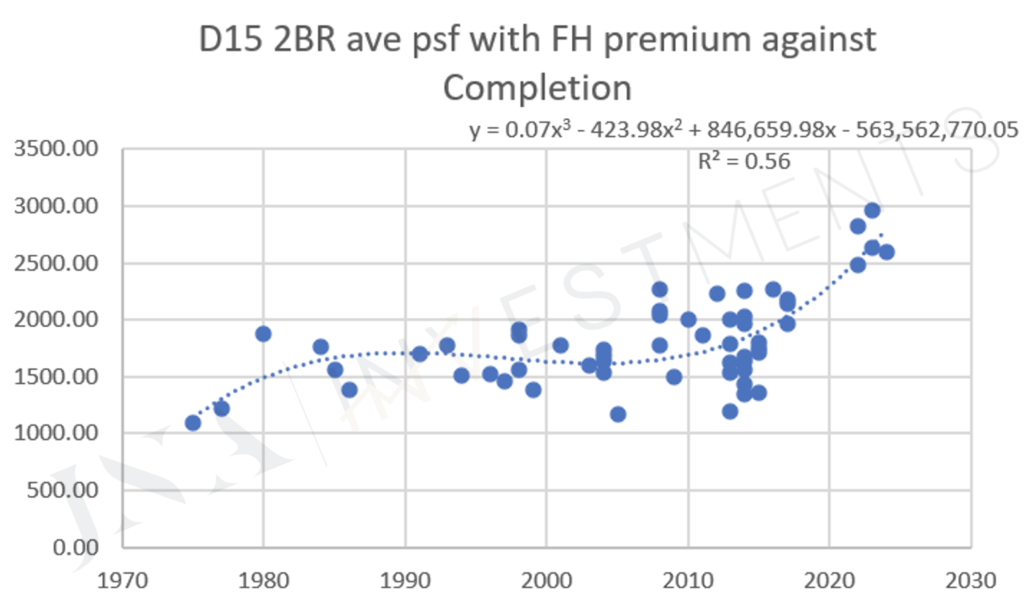

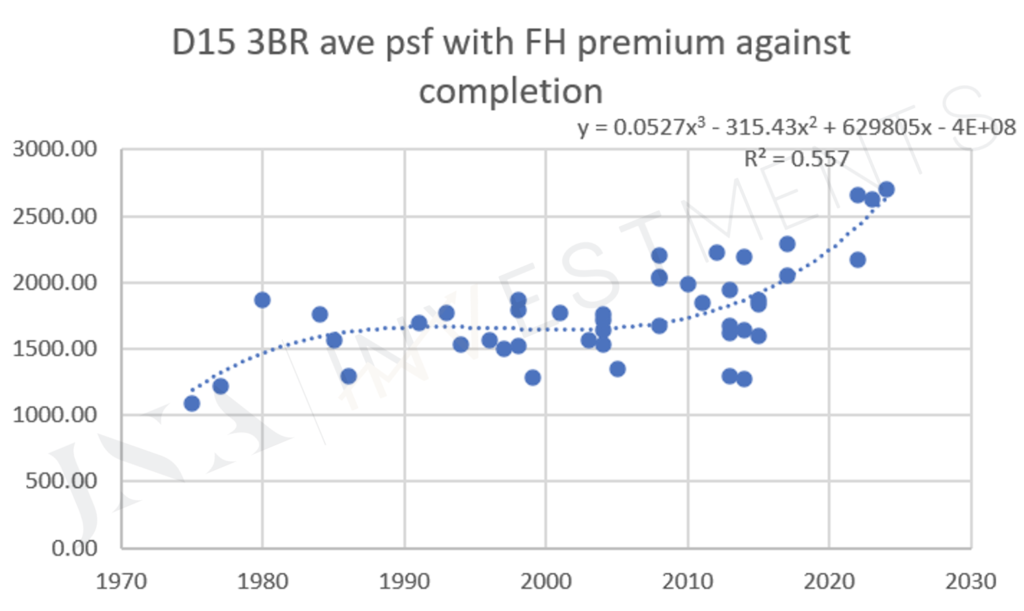

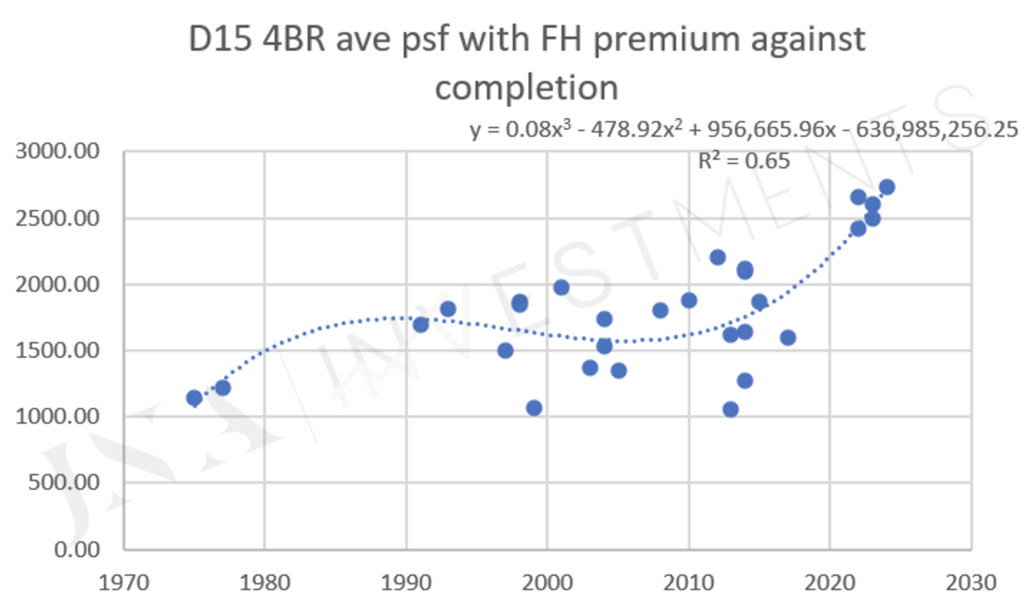

Next, using the average prices in District 15 as a benchmark (as of March 2023), adjusted for freehold price premium (i.e all the 99 leasehold developments in district 15 is added a freehold premium of 8.94%, in order to have a fair comparative between the data points), a chart is plotted for completion date against the individual average prices of all Condominium developments in D15 (as of March 2023) larger than 80 units. The reason why smaller developments are excluded is due to the variability of transaction prices in these developments that lowers its predictive accuracy.

A polynomial line of best fit (to the 3rd degree order) is drawn in order to estimate the current valuation of The Continuum based on completion date.

Following the trendline below, the estimated price for a 99-year leasehold in District 15 reaching completion is determined as such:

Source credit: JNA Investments

*Note that the lower the R square, the higher the variance in prices, and the less precise the prediction will be based on the average trend line.

Applying the trendline for each bedroom available, we can estimate based on current prices the future valuation for the average D15 FH units completed in 2027 (average 4 years to completion) and the total capital gains from the indicative starting prices as follows:

-

1BR (49 dev) FH: $2994 (2%)

-

2BR (57 dev) FH: $3281 (10%)

-

3BR (46 dev) FH: $3023 (3%)

-

4BR (30 dev) FH: $3235 (9%)

Valuation method 2: Comparing most similar development(s)

We can estimate the future price of The Continuum after completion by comparing the percentage difference between the initial launch and the highest volume transacted resale price of Condos in D15 (accounting for freehold price premium when comparing FH developments). Out of the available surrounding developments, 3 of the most recent medium – large size developments are shortlisted and their capital gains are compared.

Similar condo application 1: Amber Park (592 units, 2023, FH) (not yet completed)

The actual average launch price of each bedroom size since the launch at Amber Park is as follows:

-

1BR: Nil

-

2BR: $2506

-

3BR: $2467

-

4BR: $2444

If the equation is applied, it would be noticed that Amber Park has the following intrinsic value (with total capital gains):

-

1BR: Nil

-

2BR: $2651 (6%)

-

3BR: $2528 (2.4%)

-

4BR: $2574 (5%)

The actual latest price and capital gain since the launch at Amber Park are as follows:

-

1BR: Nil

-

2BR: $2506 to $2452 (-2%)

-

3BR: $2467 to $2753 (12%)

-

4BR: $2444 to $2418 (-1%)

It is worth noting that Amber Park has yet to TOP, and the latter prices are based on the latest new sale prices rather than resale prices, which could affect results. Nonetheless, Amber Park is used as it is the closest comparison in terms of total unit recency, and the trendline shows that Amber Park would not be a great choice for investors.

Similar condo application 2: Seventy St Patrick’s (186 total units, 2017, FH):

The actual average launch price of each bedroom size at Seventy St Patrick’s is as follows:

-

1BR: NIL

-

2BR: $1674

-

3BR: $1624

-

4BR: $1509

Based on the equation applied, it is noticed that Seventy St Patrick’s has the following intrinsic value (with total capital gains):

-

1BR: NIL

-

2BR: $2031 (21%)

-

3BR: $2029 (25%)

-

4BR: $ 1940 (29%)

The actual (highest volume) resale price and capital gain since launch at Seventy St Patrick’s are as follows:

-

1BR: NIL

-

2BR: $1674 to $1977 (18%)

-

3BR: $1624 to $2073 (28%)

-

4BR: NIL

Even though Seventy St Patrick’s is the closest to The Continuum in terms of development size and most recent TOP, it is still a much smaller development than The Continuum. This affects the quality of facilities, pricing, transaction volumes, reliability, and other factors, making it relatively less reliable as a predictor of appreciation for The Continuum, as compared to using Seaside Residences as a predictor for Tembusu Grand. More likely than not, given that The Continuum is the largest new FH development in the area, projections may be underestimated. As such, a more in-depth analysis of the qualitative aspects of The Continuum would be beneficial to determine if it is a good buy for investors.

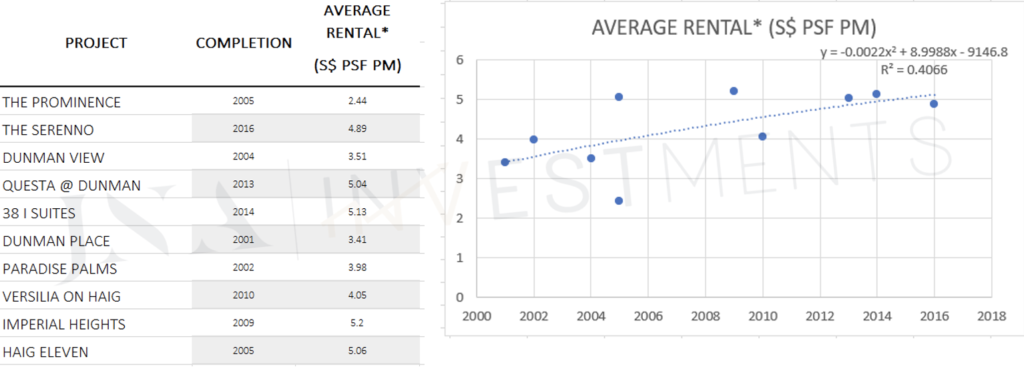

Rental Yield after completion

$psf per month can be estimated based on surrounding projects. Notably, Tenants’ demand for rental tends to be unaffected by tenure since there’s no added value of a freehold development to them.

Source credit: JNA Investments

Source credit: 99.co

Based on this trendline, the estimate current $psf pm for The Continuum would be $5.74 psf per month. Assuming the above resale projection average of $3133psf, as well as a conservative year on year average rental psf pm increase of 10% (actual 17% for last 3 years) rental yield would be estimated, in 4 years time upon TOP, at $8.036psf pm, or 3.1% rental yield, which is not the best. This assumes that demand for the Continuum as rental choice for tenants are not particularly high for any specific reason other than the development being new, which is something we can look into more in depth under fundamental analysis.

Fundamental Analysis

It is imperative to remember that while price analysis itself serves as a solid objective guideline for determining the investment potential of a development, Real Estate is ultimately heterogeneous and can be affected by a plethora of other qualitative factors that are more difficult to accurately translate into numbers. Nonetheless, we can take a look at some of these factors to determine whether any macro factors may skew profit projections in either direction.

Master Plan transformation, future land bids

Source credit: URA Masterplan

There are currently 2 nearby land bids that were sold in 2022, one year after The Continuum. One faces the Geylang River along Dunman Road with an estimated breakeven of $2120 psf ppr (99yr) and one along Haig Road at $2037 psf ppr (FH). In terms of pricing, taking into account the freehold premium of 8.94%, the new Condo along Dunman Road would be considered pricier than The Continuum. This may have factored in the potential Geylang River facing, but whether it suffices to shift demand over to the Dunman Road condominium is rather subjective.

Personally, I would not consider the river view to be as eye-catching as other rivers in Singapore like the Punggol River which Watertown faces, or the Sengkang River near Riverside@Fernvale. The other land bid, while cheaper, is a much smaller development sitting at only 2544 sqm of land (compared to 24507 sqm for The Continuum), and with an even lower plot ratio of 1.4, it is likely to be a boutique development at around 40 units, which would not be comparable with The Continuum. As such, the first land bid, would unlikely shift demand over from The Continuum, but whether it becomes a reference price high enough to boost demand for The Continuum is uncertain and would likely depend on the former’s launch price.

Aside from this, demand and supply factors in the area can also determine whether prices eventually get pushed up. Firstly, we can take a look at the demographics of this area to see if there would be increased demand for specific unit mixes.

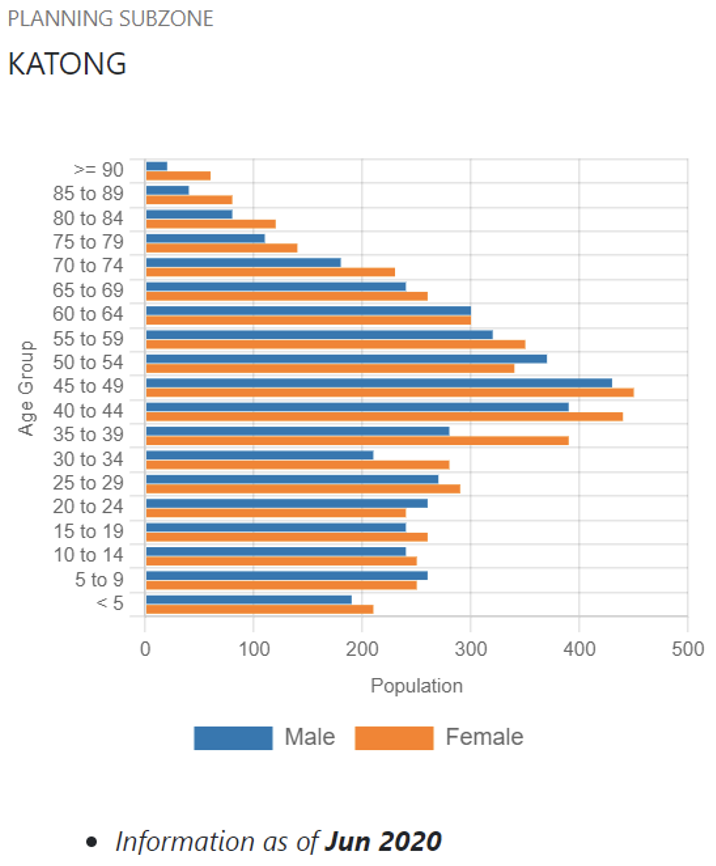

Marine Parade

Majority of Age Groups in this area are from the 40s to 50s Age range. Majority of owners at this age range likely prefer 3-bedroom units as it is at this age range where homeowners have children going to primary or secondary school and start requiring additional rooms to give privacy to their children, also would likely have saved substantial capital from working 2 decades to increase their affordability of 3-bedroom units.

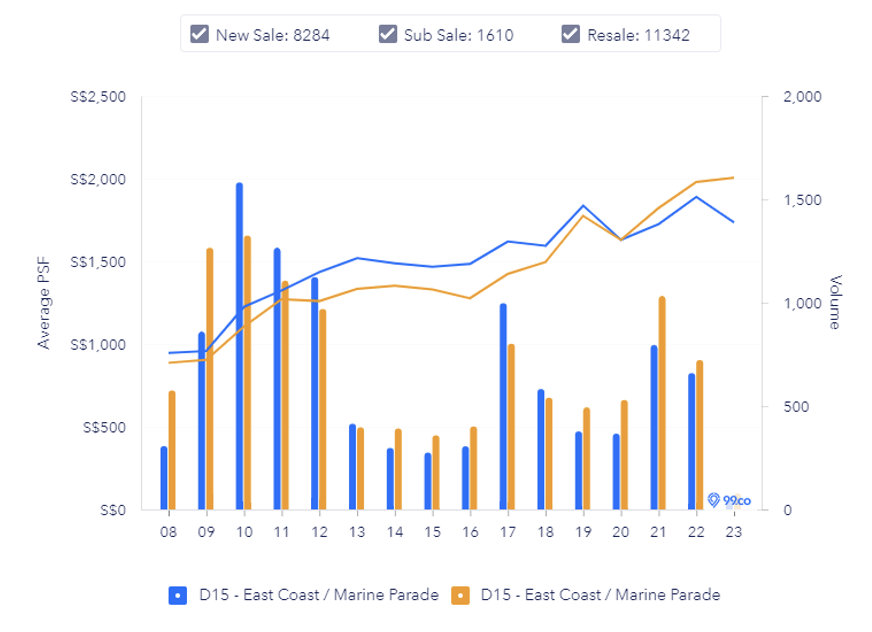

Source credit: 99.co

Already, you can see the prices (psf) of 3 and 4 bedders in D15 (yellow) have been increasing over the last few years amidst Covid as more home owners are starting to value space given the new work from home and SOHO culture, and prices have even overtaken that of smaller bedrooms. Given this information, I would prioritize larger bedroom sizes over smaller ones given similar launch prices. However, if launch prices of smaller bedrooms (specifically 2 bedders) are significantly lower than 3 bedders due to the perception of developers that 2 bedders will be harder to let go, then it could be an opportunity to purchase the 2 bedder at a significant undervalue.

Source credit: The Continuum

Another factor that could contribute to projections being underestimated is the facilities given the large land size and economies of scale. Relative to other developments around the area, the advantage of its size and quality of facilities would be a strong selling point for buyers looking for long term stay or as a long-term investment, which so happens to be the predominant age demographic of the 50s. There are however only a few unique facilities like the library, jacuzzi cove and multipurpose court that pales in comparison to Tembusu Grand’s unique facilities tailored to families with younger children, and would not likely attract younger families, in addition to being further from good schools.

Source credit: URA Space

Referring to the URA space map above, we can also see potential rental demand come mostly from the commercial stretch along Joo Chiat Road and Parkway Parade, and slightly further up north around Paya Lebar Quarter. Students attending nearby schools are more likely to choose the closer and lower cost Tembusu Grand, and with a lower psf, Tembusu Grand would likely attract a larger tenant pool and yield the highest rental returns.

Supply

D15 is still a district with high growth potential with the relocation of Paya Lebar Airbase from 2030 inviting the birth of a new generation town in the East. That said, there is no alternative like the Continuum in the surrounding vicinity, with the closest being 38 I Suites at 120 units and Questa @ Dunman at 122 units.

In terms of newest launched similar-sized Condo competitor, of course would be Tembusu Grand. As mentioned above, the factors differentiating them would be tenure, target audience and developer reputation (CDL being the better known for quantity and quality). However, if the launch price is as estimated at $2938 psf, the price difference would be significant enough to make Tembusu Grand the clear winner. Where there are many alternatives to FH Condominium (and its accompanying prices), the lack of lower priced large 99yr leasehold condominiums in the area would attract more buyers with limited budget to pick Tembusu Grand as their choice of residence upon TOP in 4-5 years time. That said, The Continuum would still attract buyers looking for longer term stay or long term investment and wishes to enjoy staying in a large compound,

Conclusion

In summary, through the use of both technical and fundamental analysis, it is our opinion that launch prices at $2600 could make The Continuum viable as an investment product as it would be priced similar to the 99-yr leasehold Liv@MB, shifting demand from Liv@MB. However, we will not likely recommend anything beyond $2800, both for those looking to flip upon TOP and those looking to rent out their units for a couple years after TOP. Nonetheless, The Continuum could be viable for those looking for long term stay or a long-term investment as, unlike Tembusu Grand, its land value does not erode over time, and there is no competition for The Continuum in terms of very large FH surrounding Condos. Lastly, it is worth keeping a lookout for the possibility of developers dropping prices significantly one or two months after launch as in the case of Sophia Hills, which could make The Continuum viable again as an investment product.

Written by: Caleb Phee | JNA Investment Analyst

Edited by: Jervis Isaiah Ng | Founder & Christian Oh | Director of Investments