The tender for Tembusu Grand under the Government Land Sales program has been closed after City Developments (CDL) placed a top bid of $768 million, equivalent to $1,302 psf per plot ratio (psf ppr). The winning price has topped the initial land value in the prime city area at $1,129 psf ppr for the Northumberland Road property that the same company bought. Tembusu Grand, a 99 leasehold site, sits in a total suite area of about 210,545 sq ft and a maximum Gross Floor Area (GFA) of 54,789m2. And with a gross plot ratio of 2.8, Tembusu Grand is expected to house 640 exquisite residential units, a midsized project for the giant property company CDL.

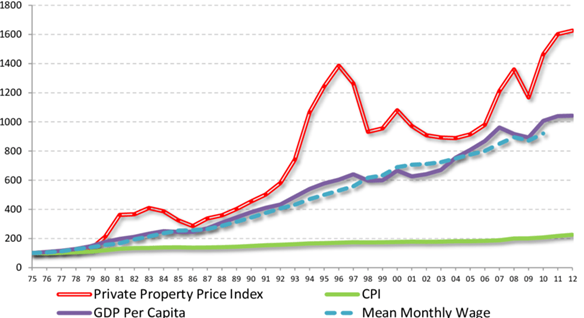

Any seasoned real estate investor would tell you, of all the factors that may affect potential capital gains, price is still king, and it is true. However, some have the misconception that a good investment purchase, based on the metric of price, is simply buying when prices have dropped below the historical average (which they determine to be intrinsic value) and selling when prices rise above that threshold. This cannot be further from the truth. Even though the product itself does not change, the intrinsic value of a development is dynamic – it is affected by present and future demand and supply, old and new surroundings and nationwide competition, government regulations, economic conditions, and a myriad of other factors. If the intrinsic value of the real estate was static, in theory, the Property Price Index (PPI) should on average increase proportionally to GDP per capita or the Consumer Price Index, which is not the case:

Source credit: Researchgate.net

As such, the determination of the intrinsic value of a property should be done through an objective method of valuation taking into account surrounding property prices that are time adjusted and subsequently supplemented by a fundamental analysis of qualitative factors that can shift projections in either direction. As such, this article will include both technical and fundamental analyses of Tembusu Grand and come to a conclusion for the price at which we view would constitute a worthwhile investment.

Technical Analysis – Estimate launch price based on comparative land bid breakeven and launch prices

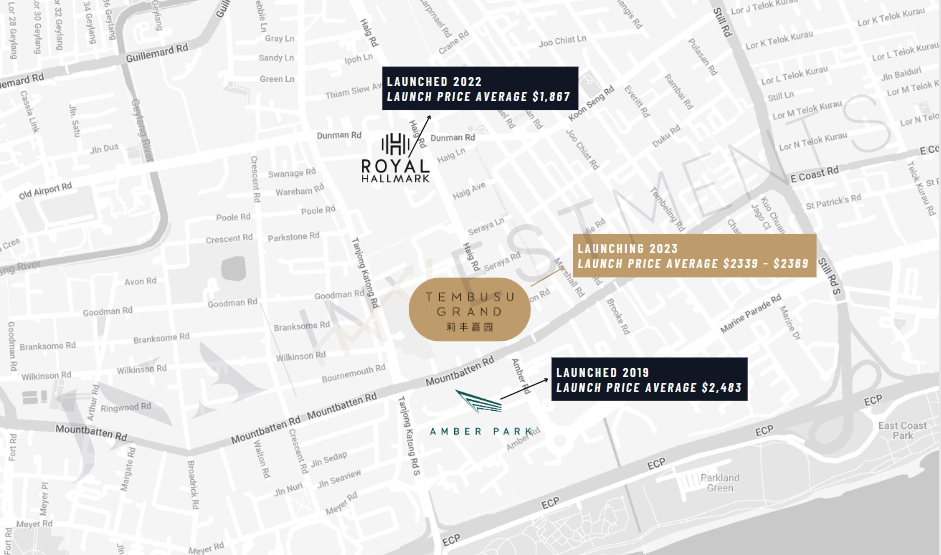

The purpose of the land bid price is to find a gauge for what is likely to be the launch price, as well as determine the rough threshold leeway for developers to drop prices subsequently should demand be lower than expected, as developers have to maintain a minimal profit margin. Here is a comparison of surrounding land bids and launch prices as well as CDL’s recent launch prices to estimate the average launch price of Tembusu Grand:

Nearby recent land bid and launch price:

2020 land bid: Haig Lane (Royal Hallmark) (Freehold), breakeven $1,589 psf, launched 2022, launch price average $1,867 (difference: 17%, $278psf)

(*Also by CDL) 2017 land bid: Amber Park (Freehold), breakeven $2,171 psf, launched 2019, launch price average $2,483 (difference: 14%, $308 psf)

Latest by CDL

2020 land bid: Irwell Bank Road (Irwell Hill Residences) (99yrs), breakeven $2,331, launch price $2,633 (difference: 13%, $302 psf)

2018 land bud: Sengkang Central (Sengkang Grand Residences) (Mixed, 99yrs), breakeven $1,462, launch price $1748 (difference: 19%, $286 psf)

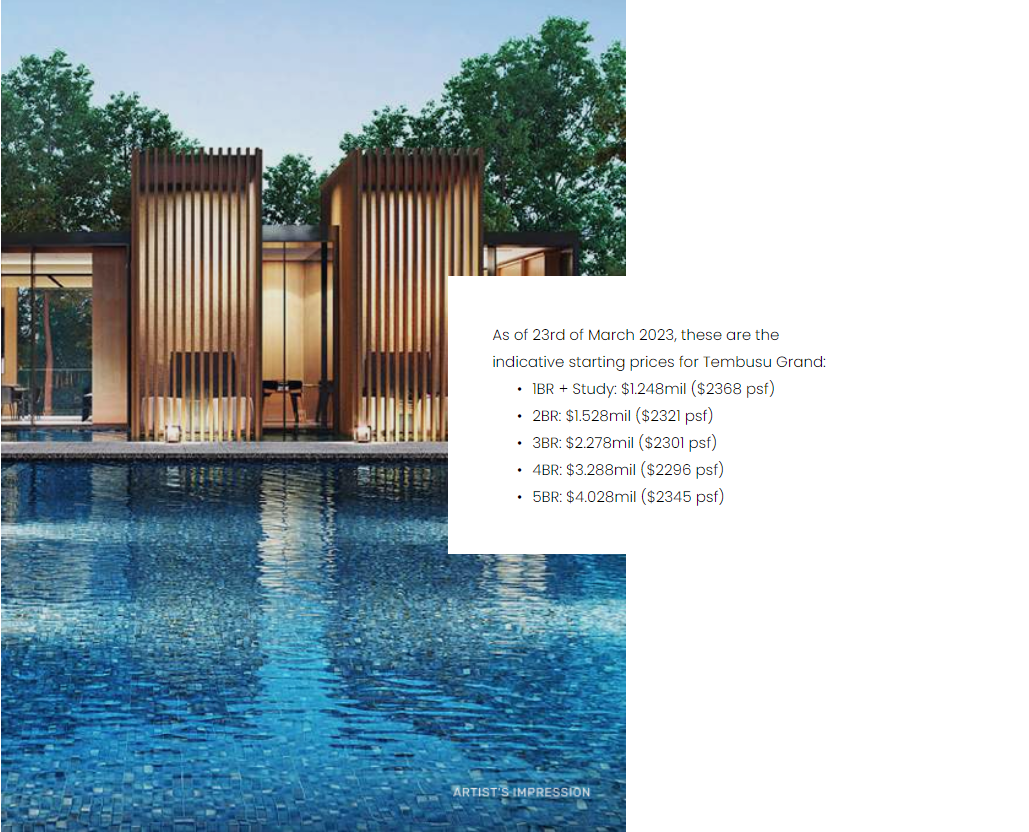

Given an estimate of around $280psf – $310psf difference between estimate breakeven and launch price, with Tembusu Grand’s breakeven estimated at $2059, launch price average would likely lie between $2339 to $2369 psf (difference: 14-15%)

Estimated Capital Gain

For the purposes of estimating capital gains, each bedroom size will have its analysis to avoid skewed average prices of developments as a result of differing bedroom size mixes.

Valuation method 1: Estimation based on average prices and completion date

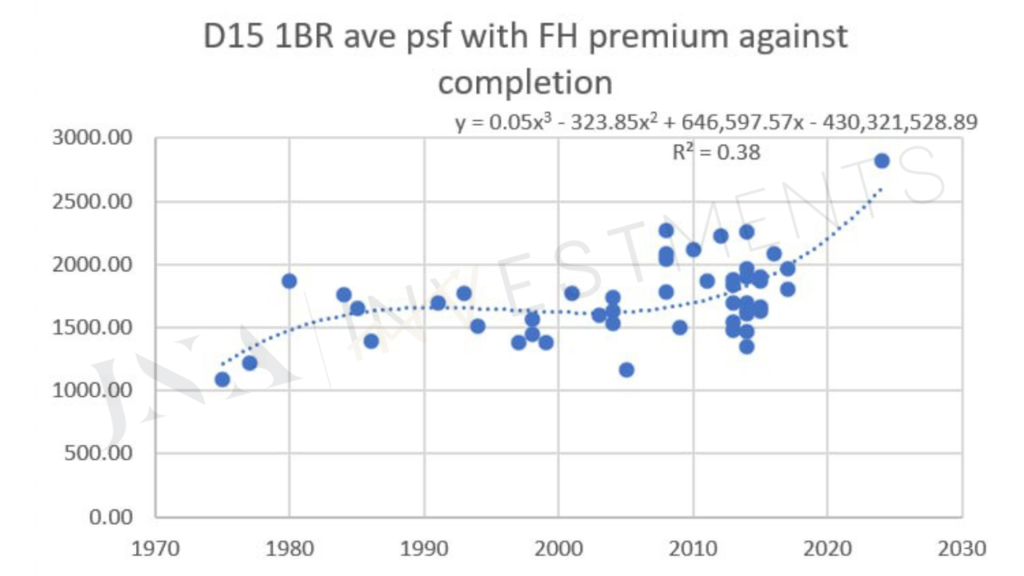

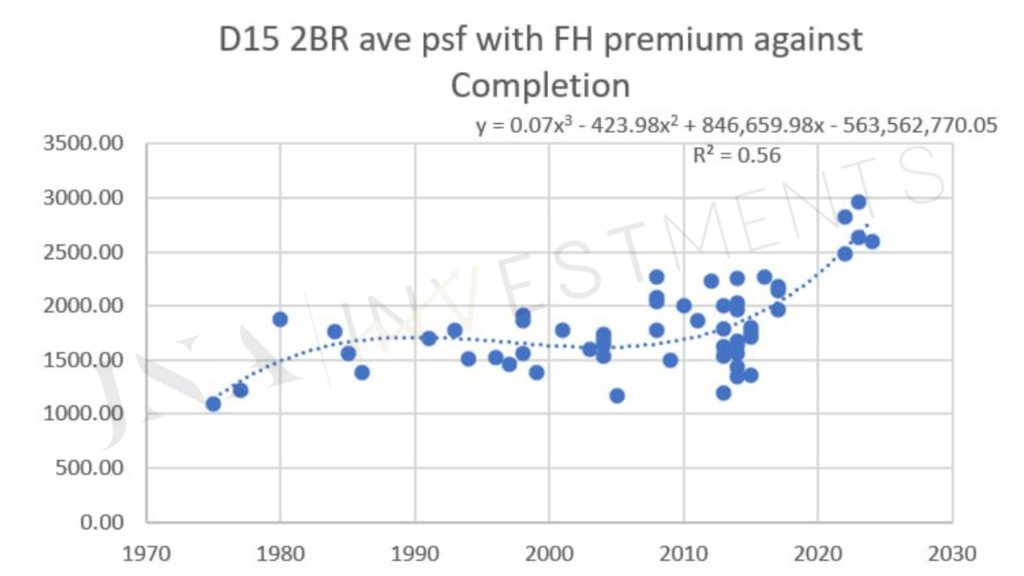

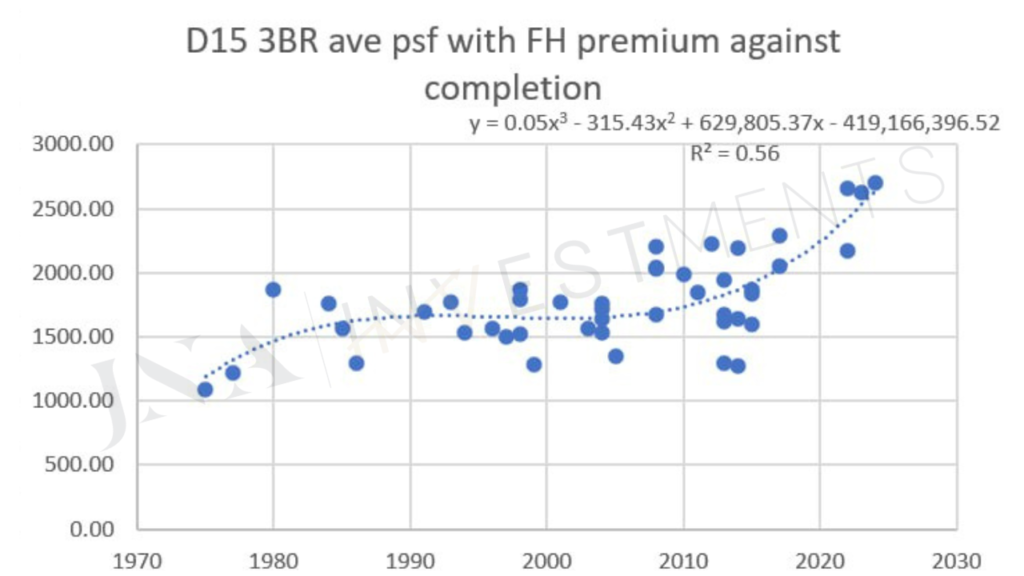

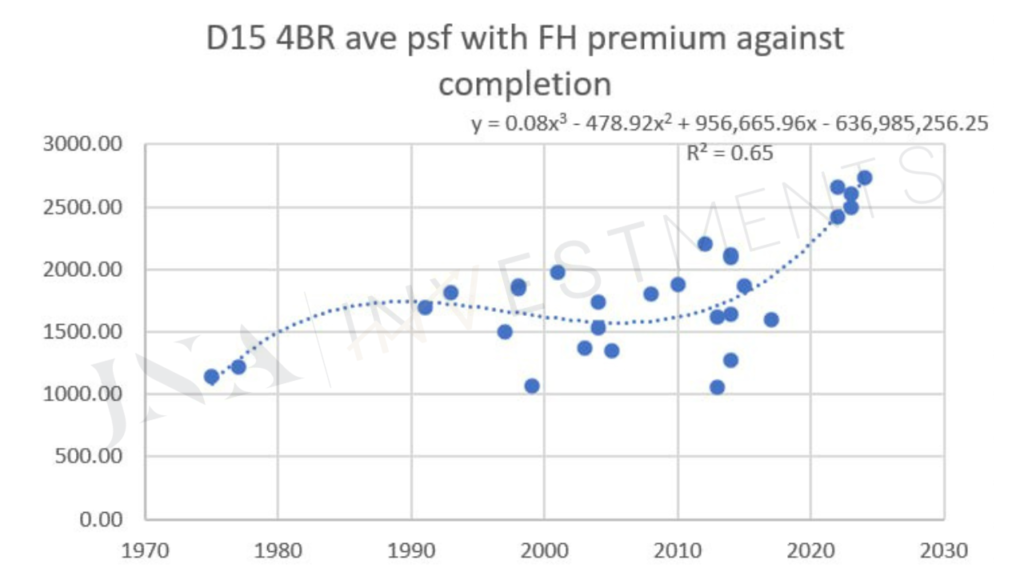

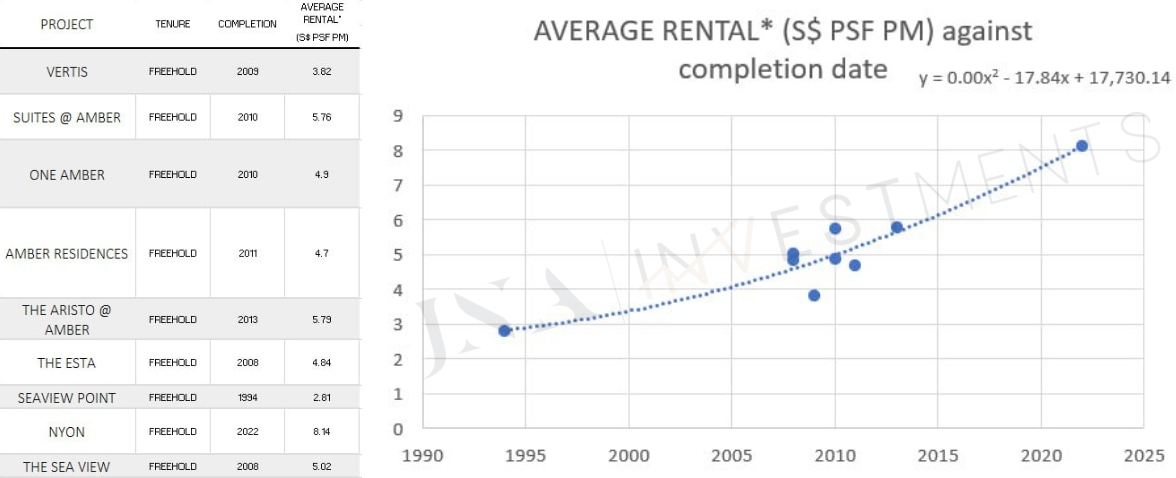

This valuation method is applied by plotting a graph of average prices against the completion year (TOP date), for which we can find the estimated intrinsic value of the property unit for each unit type in the district based on when it is completed. The key is to purchase a unit at a reasonably below the estimated intrinsic value to enjoy capital gains.

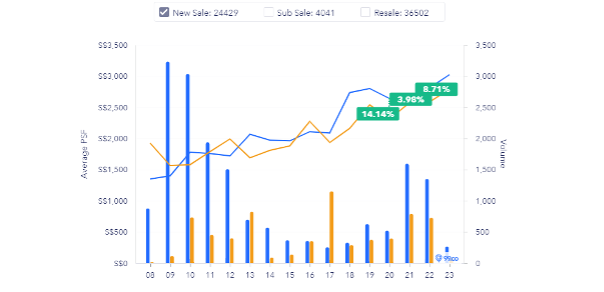

Firstly, we can estimate freehold premium by finding the 3-year average of the difference in average prices of 2BR with Freehold and 99yr leasehold tenure (for new sale). It is imperative to note the unique nature of D15 being overwhelmingly a freehold district, unlike some other areas, meaning that the premium buyers are willing to pay for a freehold tenure development in these areas are diminished. In order to more accurately measure freehold premium in a district dominated by freehold Condos, the average district new sale prices of districts 9, 10 and 15 will be used.

Source credit: 99.co

Looking at the most recent 3-year average new launch prices for 99-yr and freehold condos, we can estimate the recent value of freehold premium in D15 to be:

(14.14% + 3.98% + 8.71%) / 3 = 8.94% (lower than the nationwide average freehold premium of 18.7%)

Next, using the average prices in District 15 as a benchmark (as of March 2023), adjusted for freehold price premium (i.e all the 99 leasehold developments in district 15 is added a freehold premium of 8.94%, in order to have a fair comparative between the data points), a chart is plotted for completion date against the individual average prices of all Condominium developments in D15 (as of March 2023) larger than 80 units.

A polynomial line of best fit (to the 3rd degree order) is drawn in order to estimate the current valuation of Tembusu Grand based on completion date. The reason why smaller developments are excluded is due to the variability of transaction prices in these developments that lowers its predictive accuracy.

Following the trendline below, the estimated price for a 99-year leasehold in District 15 reaching completion is determined as such:

*Note that the lower the R square, the higher the variance in prices and the less precise the prediction will be based on the average trend line.

Applying the trendline for each bedroom available, we can estimate based on current prices the future valuation for the average D15 FH units completing in 2027 (average 4 years to completion). Subtracting the average freehold premium estimated at 8.94%, the valuation of an average D15 99-year leasehold completing in 2027 and the total capital gains from the indicative starting prices would be estimated as follows:

1BR (49 dev) — FH: $2994 99yr: $2726 (15%)

2BR (57 dev) — FH: $3281 99yr: $2987 (28%)

3BR (46 dev) — FH: $3023 99yr: $2752 (20%)

4BR (30 dev) — FH: $3235 99yr: $2946 (26%)

Valuation method 2: Comparing most similar development(s)

We can estimate the future price of Tembusu Grand after completion by comparing the percentage difference between the initial launch and the highest volume transacted resale price of Condos in D15 (accounting for freehold price premium when comparing FH developments). Out of the available surrounding developments, only 2 medium-large developments were launched relatively recently with 99-yr leasehold tenure, out of which only Seaside residences have TOPed. As such, Seaside Residences would be the most appropriate to compare an estimate of appreciation from launch to completion.

*Similar Condominium Application

Seaside residences, a total of 841 units, 99-year leasehold

Seaside residences, a total of 841 units, 99-year leasehold

The actual average launch price of each bedroom size at seaside residences is as follows:

1BR: $1776 2BR: $1723

3BR: $1648 4BR: $1741

Based on the equation applied, it is noticed that seaside residences (99 years) have the following intrinsic value (with total capital gains):

1BR: $2292 *91.06% (FH premium) = $2087 (17.5%)

2BR: $2405 *91.06% (FH premium) = $2189 (27%)

3BR: $2332 *91.06% (FH premium) = $2123 (28%)

4BR: $2319 *91.06% (FH premium) = $2112 (21%)

The actual total appreciation of each bed size average price from launch to resale:

1BR: $1776 to $2120 (16%)

2BR: $1723 to $2095 (22%)

3BR: $1648 to $2110 (28%)

4BR: $1741 to $2180 (25%)

It is worth noting that for Seaside Residences, even though it showed the highest appreciation, it also had a significantly lower starting price compared to the other bed sizes, as compared to the starting prices for 3 bedders in Tembusu Grand. Nonetheless, based on these 2 methods of valuation, for investment purposes, we would prioritise the following bed sizes for maximum capital appreciation (%) based on our final estimation:

1. 2 or 4 BR (24 – 28%)

2. 3 BR (22 – 26%)

3. 1 BR (15% – 18%)

*The graphs are based on current prices and the best-fit trendline and hence projected price would differ slightly when measured in previous years.

Rental Yield After Completion

$psf per month can be estimated based on surrounding projects. Notably, Tenants’ demand for rental tends to be unaffected by tenure since there’s no added value of a freehold development to them.

Based on this trendline, the estimate current $psf pm for Tembusu grand would be S$9.81 psf pm, or $117.72 psf per year.

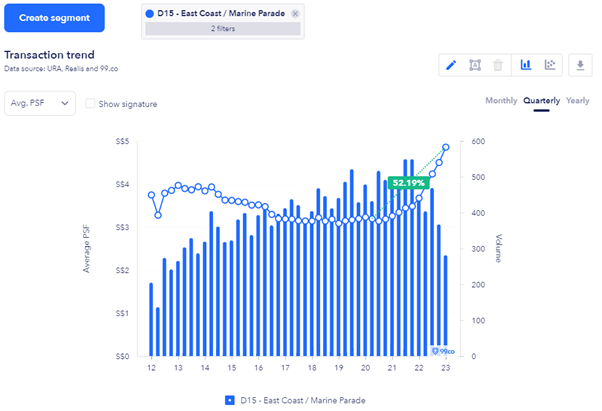

Source credit: 99.co

The average percentage increase in rental psf from 2020 to 2023 is 52.19%, which averages to around 17% per year. Based on this projection, the average rental for Tembusu Grand upon completion would be 168%*$9.81psf pm which is $16.48 psf pm, or $197 psf per year for an average $3231 psf unit, equating to 6% rental yield in 2027.

It is worth noting that rental prices have increased at an absurd rate in the last 3 years in light of Covid-19, which may skew future projections, especially with the possibility of new government policies implemented in the future to curb the increase in rental prices.

Fundamental Analysis

It is imperative to remember that while price analysis itself serves as a solid objective guideline for determining the investment potential of development, Real Estate is ultimately heterogeneous and can be affected by a plethora of other qualitative factors that are more difficult to accurately translate into numbers. Nonetheless, we can take a look at some of these factors to determine whether any macro factors may skew profit projections in either direction.

Master Plan transformation, future land bid

The most recent land bid that has been open for tender (until 18 July 2023) is a 3.5 PR land plot just across the road from Tembusu Grand. If the successful bid price for the land plot far surpluses that of Tembusu Grand, it could potentially increase demand for its direct competitor, or at worst provides a safety net for ensuring prices at Tembusu Grand do not drop too significantly.

Historically, the presence of new launches has often pushed up prices of surrounding Resale Condo developments by setting the benchmark price in a particular area – one clear example is High Park Residences, which launched in 2015 at around $980psf. From 2015 to 2017, the average new launch prices at High Park Residences increased only 0.77% and fluctuated around $1000psf. It was not until 2018 with the new launch of the nearby Parc Botannia at $1283 psf on average (300 psf higher) which set the reference price in the area and shifted demand towards High Park as a comparable but much cheaper alternative, causing new launch prices to rise to an average $1276 psf, only $60psf less than Parc Botannia.

Source credit: 99.co

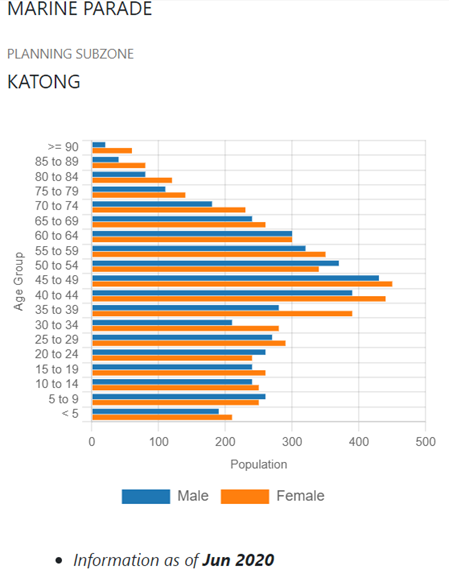

Aside from this, demand and supply factors in the area can also determine whether prices eventually get pushed up. Firstly, we can take a look at the demographics of this area to see if there would be increased demand for specific unit mixes.

Source credit: Masterplan

The majority of Age Groups in this area are from the 40s to 50s Age range. The majority of owners at this age range likely prefer 3 bedroom units as it is at this age range where homeowners have children going to primary or secondary school and start requiring additional rooms to give privacy to their children, also would likely have saved substantial capital from working 2 decades to increase their affordability of 3 bedroom units.

Tembusu Grand Site Plan

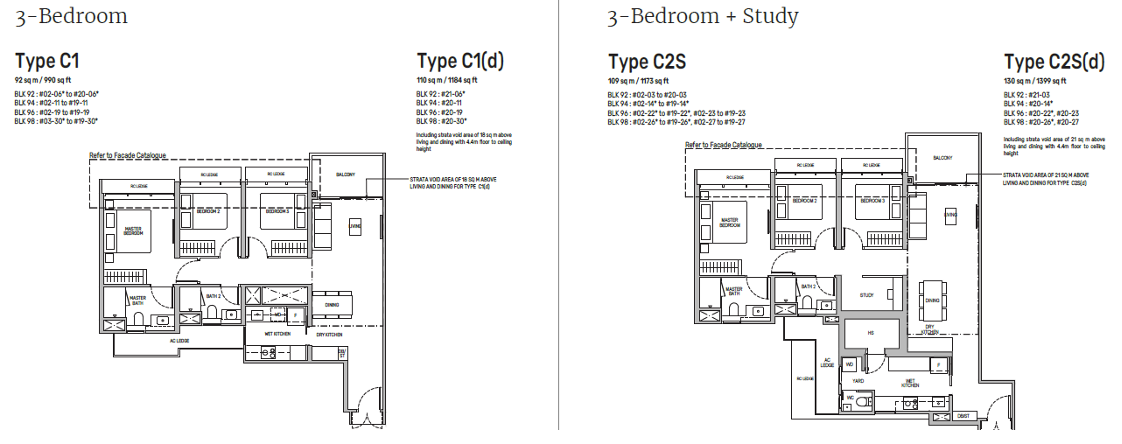

What stands out is how Tembusu Grand’s facility and unit mix tailors mainly to their target groups of young families – we can see specific facilities that tailor to young children like a wading pool, relaxing pool, playhouse, kid’s playroom, play dom, gaming pods, as well as karaoke rooms for family leisure. More importantly, we can see from the unit mix that the predominant unit size is 3 bedrooms + study, which doubles the number of 1 bedroom + study and 2 bedders. Not to mention, the area is surrounded by many good secondary schools like Chung Cheng High School and Tanjong Katong Girl’s School and Secondary School, as well as being a stone’s throw away from East Coast Park which is an added incentive for families of this age range to reside there.

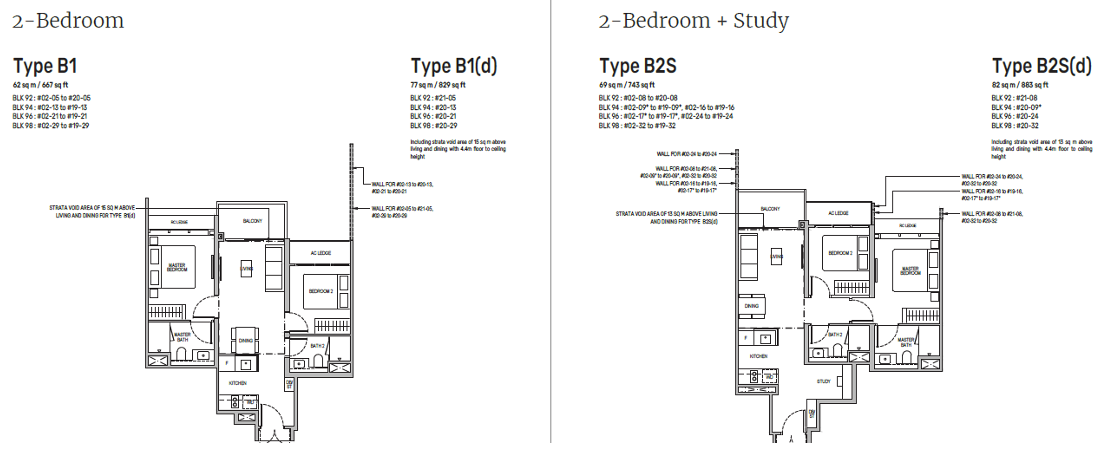

Tembusu Grand 3-bedroom & 3-bedroom + study floorplan

Tembusu Grand 3-bedroom & 3-bedroom + study floorplan

Tembusu Grand 2-bedroom & 2-bedroom + study floorplan

The unit layout will also appeal to buyers as it is efficiently shaped with most spaces fully utilized. However, it is worth noting that certain unit layouts with a “(d)” include a strata void area above the living and dining area or the normal 3 bedrooms with a void area behind the wet kitchen, if not accounted for as a discount in launch price from units without wasted void area, would likely be sold upon completion at a lower quantum than those without wasted space.

Referring to the URA space map above, we can also see potential rental demand come not only from students from the many educational institutions nearby, but also from working tenants coming from the commercial stretch along Joo Chiat Road and Parkway Parade, or even slightly further up north around Paya Lebar Quarter.

Supply

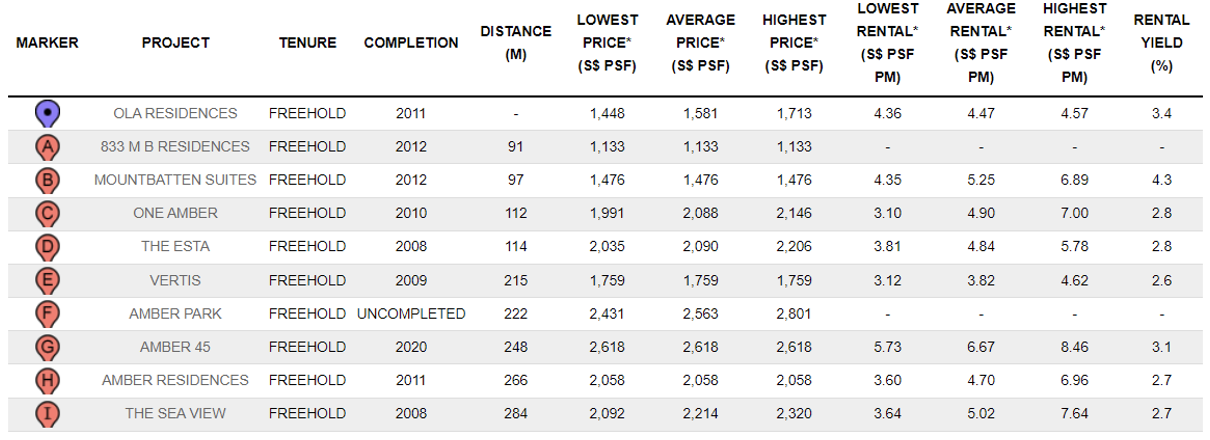

While D15 is still a district with high growth potential with the relocation of Paya Lebar Airbase from 2030 inviting the birth of a new generation town in the East, Tembusu Grand is still almost surrounded by Condo supply, and worse still is a 99-year leasehold in a freehold enclave.

Source credit: Squarefoot

In terms of the newest launched similar-sized Condo competitor, the most prominent is Liv@MB, a 390 unit 99-year leasehold Condominium with 40 remaining units (majority 1200 -1300sqft 3-bedders) going at an average of $2640 psf with an estimated completion date of 2024 – 2025, which is similar in size to the 3 Bedroom + Study unit in Tembusu Grand. With this in mind, it is more likely if prices were to be launched similarly at 2600psf for the similar-sized 3BR + S units, buyers may turn to Liv@MB instead with the preferred FH tenure.

It will also likely compete with the upcoming new launch at D15, The Continuum (816 units), which has a land bid breakeven estimated at $2296psf, $250 psf more than Tembusu Grand but sold with Freehold Tenure, which is less than the average estimate freehold premium of 18.7%

That said, to a future buyer looking at a shorter term own stay, a 99yr leasehold may not be a big concern, in which case upon reaching TOP, Tembusu Grand would likely be highly demanded purely based on being lower priced than its freehold alternatives, albeit likely capped near prices of more recently TOPed Freehold Condominiums in the area like Liv@MB.

In summary, through the use of both technical and fundamental analysis, it is our opinion that launch prices at $2300 – $2400 + would make Tembusu Grand a clear investment choice, but will not likely recommend units going at $2500 – $2600. In terms of profit gain, 2 to 4 bedrooms would likely gain between 20% to 28%, while 1 bedroom performs slightly worse as an investment at 15% to 16% total capital gains. Unit layouts like the 3 bedroom classic or unit types with (d) that have void spaces should also be avoided if priced similarly to layouts like 3 bedroom + study that have better utilized space. In comparison to The Continuum, supply of low quantum developments is D15 is much rarer and would likely attract more demand for those looking to live near East Coast Park with at a more affordable price.

Written by: Caleb Phee | JNA Investment Analyst

Edited by: Christian Oh | Director of Investments